The Germany CSRD implementation marks a significant step in aligning national corporate governance with the European Union’s Corporate Sustainability Reporting Directive (CSRD). The German government has introduced a draft CSRD Implementation Act, which proposes sweeping legal changes across commercial, corporate, securities, and auditing laws to ensure compliance with EU sustainability standards.

The reforms aim to make sustainability reporting a central element of corporate accountability, focusing initially on large, listed companies before expanding to other sectors over the next several years.

Key Features of Germany CSRD Implementation

The Germany CSRD implementation introduces extensive amendments to national legislation, including:

- German Commercial Code: Updates to integrate sustainability reporting obligations

- Company and Securities Laws: Expanded duties for disclosure and corporate governance

- Auditing and Supply Chain Statutes: Enhanced verification and reporting requirements

- Board-Level Responsibility: Increased liability for directors ensuring accurate reporting

These changes ensure that German corporations adhere to both financial and non-financial reporting standards, reflecting the EU’s commitment to environmental, social, and governance (ESG) transparency.

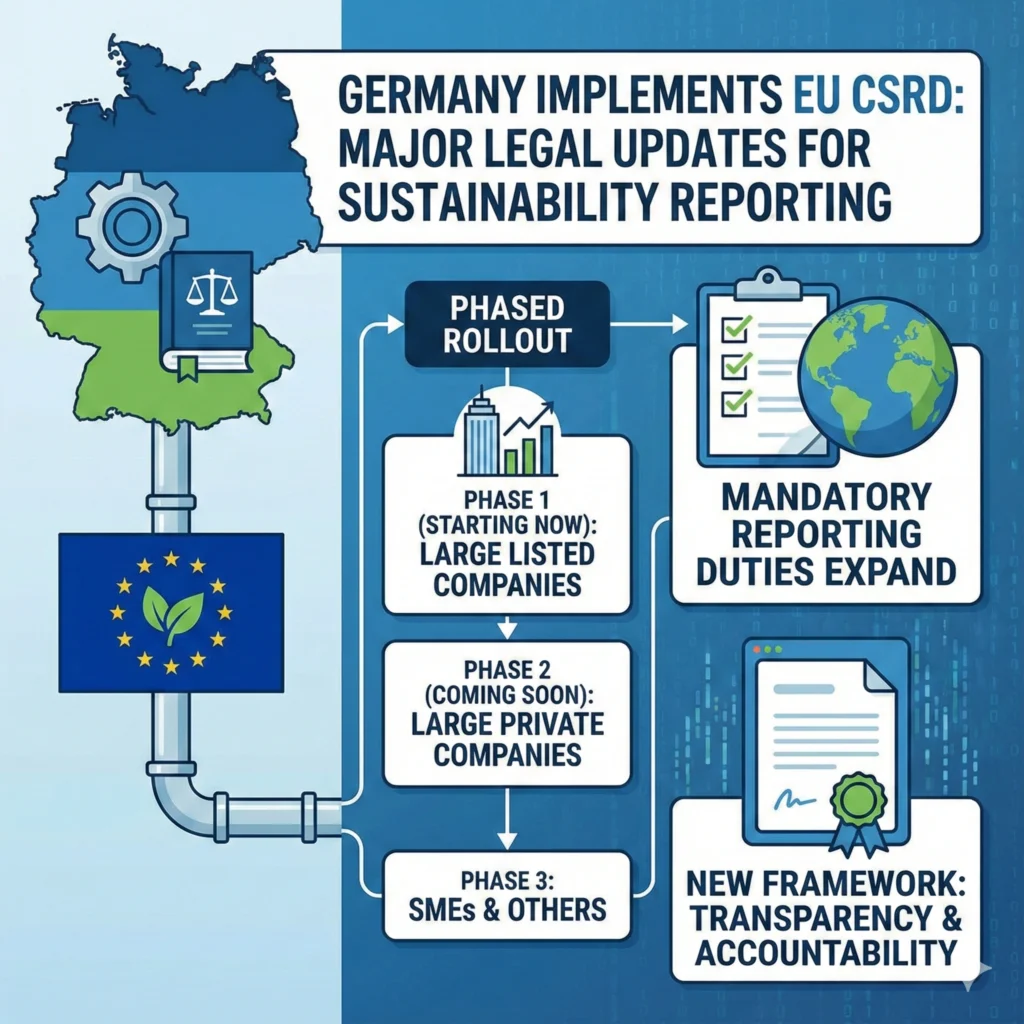

Phased Rollout of Sustainability Reporting

Under the Germany CSRD implementation plan, reporting obligations will be introduced in stages:

- 2024 Financial Year: Large capital market-oriented companies with more than 500 employees

- 2025–2028: Gradual inclusion of medium-sized and other relevant companies, following EU-defined criteria

- Group-Level Reporting: Consolidated sustainability statements for parent and subsidiary companies

This phased approach allows companies to adapt reporting systems, integrate ESG metrics, and strengthen internal audit functions before full compliance is required.

Enhanced Audit and Accountability Measures

One of the most notable aspects of Germany CSRD implementation is the tightened audit requirements. Companies will be expected to:

- Provide independent verification of sustainability reports

- Ensure board oversight of ESG compliance

- Document supply chain impacts and mitigation strategies

These measures are intended to increase transparency, reduce greenwashing, and ensure investors and stakeholders have access to reliable sustainability data.

Impact on Corporate Governance

The Germany CSRD implementation aligns corporate governance with broader EU objectives. Key impacts include:

- Director Liability: Boards can be held accountable for inaccurate or incomplete reporting

- Integrated Reporting: Sustainability metrics become part of corporate strategy, not a side note

- Investor Confidence: Standardized ESG reporting helps investors make informed decisions

Legal experts note that companies will need to adapt internal controls, data collection processes, and risk management frameworks to comply effectively.

Significance for EU and Global Sustainability Goals

Germany’s proactive adoption of CSRD standards positions it as a leader in European ESG compliance. By enforcing robust reporting rules, Germany ensures that its companies contribute meaningfully to:

- EU climate targets and carbon neutrality initiatives

- Sustainable investment frameworks

- Transparent supply chain practices

Moreover, companies operating internationally may benefit from harmonized ESG reporting across EU markets, reducing complexity and enhancing competitiveness.

Next Steps for Businesses

Businesses affected by the Germany CSRD implementation should prepare by:

- Assessing current ESG reporting systems

- Establishing data collection and monitoring processes

- Training boards and senior management on new liability standards

- Engaging external auditors for verification readiness

Early preparation will help mitigate compliance risks and ensure smooth adaptation to the new legal framework.

Source: Squire Patton Boggs

For the latest news from Germany, visit our Germany news page.